Wheat feeding is increasing as wheat and corn are near parity in some markets.

In its 2025/26 June WASDE report, the USDA is projecting China’s feed use for wheat unchanged from 2024/25 at 33 million tons.

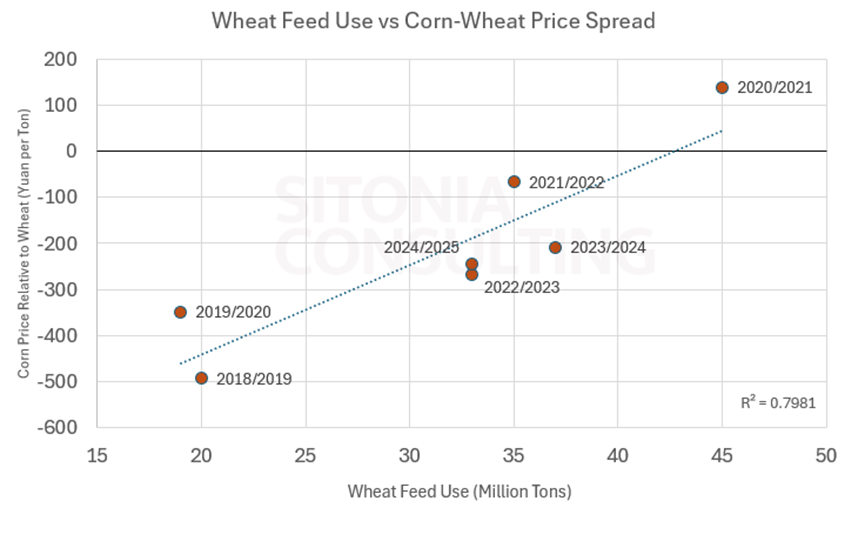

Plotted below is the price spread between wheat and corn compared to each marketing year’s estimate for wheat feeding. On the left axis is the price spread in Henan. When the line is below zero, corn cheaper than wheat, and when it’s above zero, wheat is cheaper than corn.

However, typically when wheat is at a premium of 100 yuan/ton or less it will be economical for feed mills to use wheat rather than corn.

The 2020/2021 marketing year is an outlier with corn prices at one point being 400 yuan per ton more expensive than wheat, and wheat feeding reaching 45 million tons.

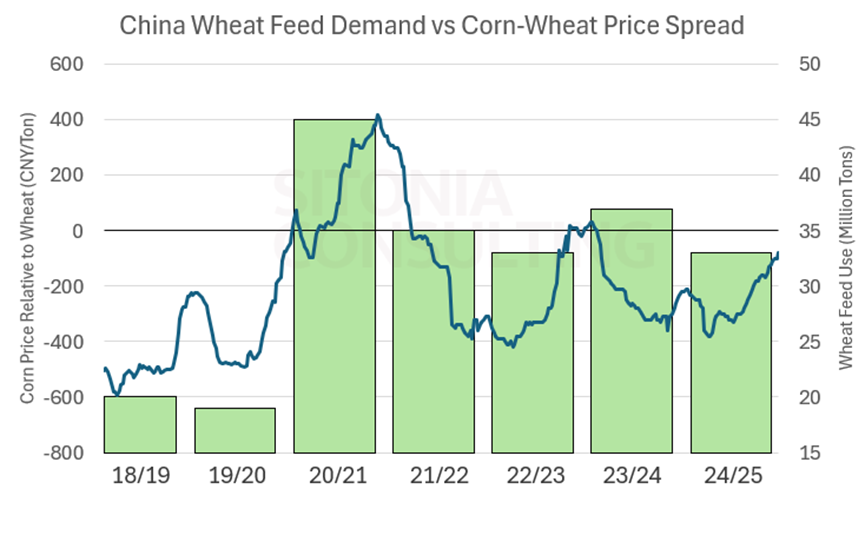

From 2016 through 2020, China had been auctioning off its temporary corn reserve that had been purchased from farmers in the years prior to support prices.

As those reserves ran out, supply shrunk, and prices rallied about 1000 yuan per ton, or 50%, from mid-2020 through mid-2021.

Since then, wheat feeding has ranged from 33-37 million tons per year. 2023/24 saw higher wheat feeding at 37 million tons due to late rains which damaged wheat crops.

Last year saw wheat feeding fall as corn prices fell and last year’s wheat crop quality was good.

The corn market is currently in a situation of tight supply as farmers have sold all of their crop earlier than last year and imports have essentially stopped.

Although China has imported some corn, imports have been below 500k tons per month for 10 months now. Prior to this, imports were above 500k tons per month for 52 consecutive months. During those 52 months, imports averaged 1.9 million tons per month.

In 2023/24, wheat was being used as feed because it was damaged, but this year, wheat is being used as feed because corn supplies are tight and prices continue to rally.

In that context, the USDA projection of 33 million tons of feed demand for wheat seems conservative and could be raised in coming months.

The tightness in the corn market could see China normalize its corn imports and depending on how much wheat ends up going to feed, also increase its wheat imports.