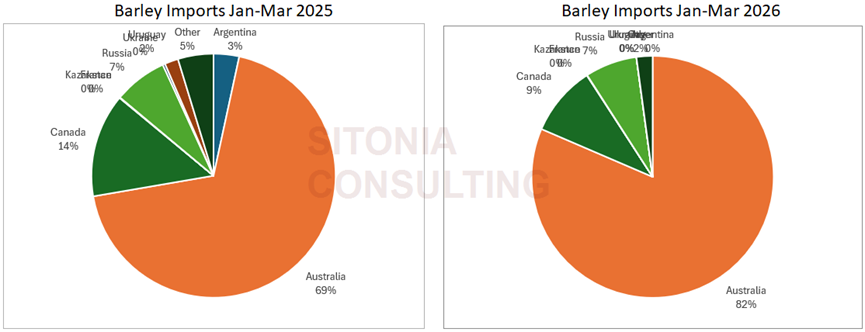

Barley imports continued to be strong in March with nearly all of this volume coming from Australia. Compared to Q1 2025, Australia has an even larger market share of barley imports at 82%.

The pace of imports has also been strong to start this year, with a total of 3.5 million tons imported, one of the strongest starts to the year.

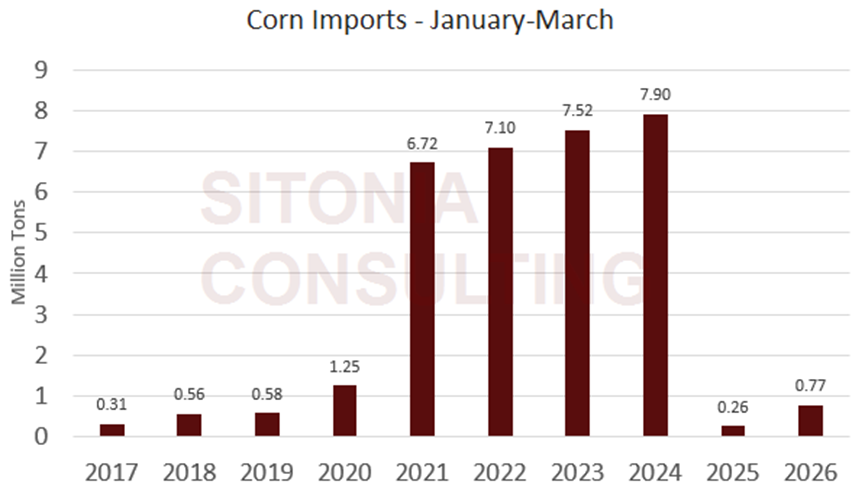

Corn imports were primarily from Brazil with accounted for 206k tons or 92% of March imports. While imports are up substantially compared to last year, they are also down dramatically compared to previous years. For example, 2024 Q1 imports were 7.9 million tons.

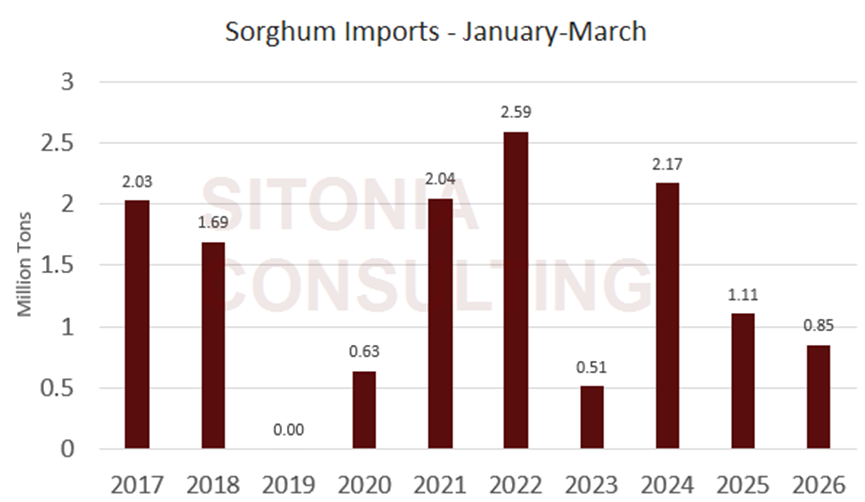

Sorghum imports are down slightly compared to last year. The US remains the largest supplier, but Argentina has gained market share. Q1 imports are at the lower end of their range.

Wheat imports are up sharply compared to last year, but similar to corn, are down compared to the 2021-2024 timeframe.

Argentine was the biggest supplier to China in March. This came after COFCO began purchasing Argentine wheat in December. China previously didn’t import wheat from Argentina.

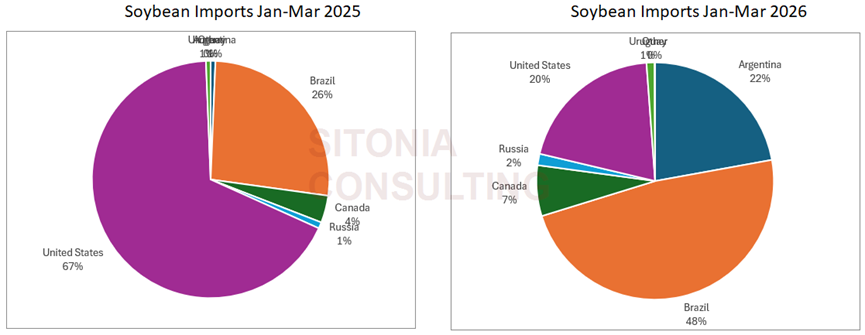

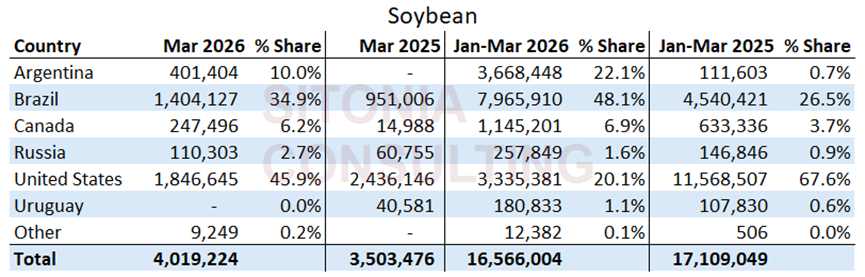

Soybean imports show a large shift in origins compared to Q1 2025, when the US was the largest supplier to China. Outside of Brazil and the US, there have been increases in imports from other suppliers. Imports from Argentina, Canada, Russia, and Uruguay all increased compared to Q1 2025.